Mr. Sanjay Chawla

Chief Investment Officer - Equity, Baroda BNP Paribas Mutual Fund.

Mr. Chawla has over 35 years of experience in fund management, equity research and Management Consultancy. Currently, he is Chief Investment Officer - Equity at Baroda BNP Paribas Asset Management India Private Limited. In his prior roles, he has worked with Baroda Asset Management India Limited as Chief Investment officer, Birla SunLife AMC as Sr. Fund Manager-Equity, managing various schemes with different strategies. Mr. Chawla has also worked as Head of Research with SBI Capital Markets and in various capacities in the equity research space in Motilal Oswal Securities, IDBI Capital Markets, SMIFS Securities, IIT Invest Trust & Lloyds Securities. He is the fund manager for certain schemes of the Mutual Fund. Mr. Chawla is graduated with a Master of Management Studies from Birla Institute of Technology & Science (BITS), Pilani.

Please note we have published the answers as it is received from the Fund Manager of Baroda BNP Paribas Mutual Fund.

Q1. Following the recent government commentary around fuel conservation, gold imports, and external vulnerabilities, do you believe long-term investors should be concerned about the broader macroeconomic impact, or are these measures largely preventive steps reflecting prudent economic management?

Ans: In our view, the recent government commentary around fuel conservation, gold imports etc is more of a groundwork towards the possibility of an extended resolution to the West Asia conflict. As the conflict lingers and the disruptions in the Straits of Hormuz continues, crude/gas/petrochemical prices remain elevated. This is likely to place a downward pressure on GDP growth, an upward bias on inflation and a worsening current account deficit (CAD) placing pressure on the currency. It makes the situation for maintaining fuel prices less and less tenable. For long term investors, the currency and bond markets (OIS markets are tentatively pricing in 50bps rate increases by the close of FY27) have already recalibrated to a large degree. Equity has seen a small bounce from the lows of March when peace talks began and market may give up those rebound gains in case a truce is delayed. However, our health as an economy as we entered into this conflict is vastly different from say the global financial crisis years or the tech meltdown years. Valuations euphoria had already drained through CY2025 and our valuations have now reverted to mildly below long term levels. FII ownership is also at a multi-year low indicating no extended ownership. Retail leverage/margin financing etc have also been manageable. Yes, growth may be vulnerable and one could see 300-500bps of earnings cuts, but it would not be meaningfully large as an extension to impact on markets. This crisis may actually be a reasonable window for long term investors to get into markets. A resolution of the conflict would naturally translate to cool off in energy markets in 1-2 quarters, changing not only sentiments but also reducing the CAD and relieving the risks to growth and inflation.

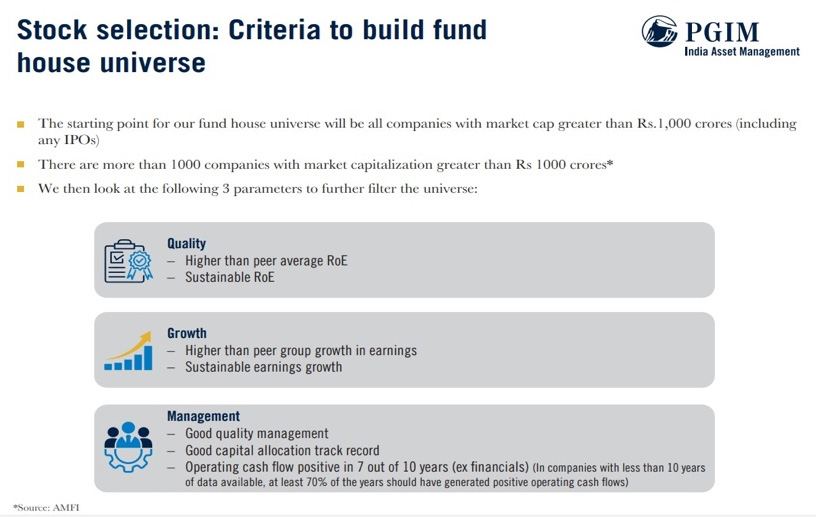

Q2. Beyond financial metrics, how do you assess the qualitative aspects of a company while filtering stocks for long-term portfolios? What are the early signs that help you differentiate sustainable compounders from businesses benefiting only from short-term cycles?

Ans: We look at a triangulation of BMV - business, management and valuation to identify long term winners. A company’s ability to weather shocks and sustain its growth can stem from multiple sources - a technology proficiency, large scale driving competitiveness, ability to leverage on raw materials (e.g. access to high grade alumina for an aluminium producer) or labour costs (certain labour-intensive jobs may be more competitive out of India) etc. The other part M - management is where we desire consistency between statements and action, proper timely execution of articulated strategy with a high level of governance and lastly the V - valuation i.e. there has to be a relation between price (we pay) and the value (we get).

Q3. Smart beta strategies are gaining ground as investors seek a middle path between passive and active investing. How do you view the growth of smart beta in India, and can factor-based strategies consistently add value across market cycles compared to traditional active and passive approaches?

Ans: These are interesting alternatives to broaden the choices available to investors. Some of these categories are quite nascent so one could see some build-up of assets in the near future. However, they have their own pros and cons. On the positive side, they may be a little cheaper and also they do eliminate some human biases. On the negative side, typical strategies like momentum or quality etc. do not work across all time frames and it may be more appropriate for an astute investor to keep shuffling across such styles. A less involved investor may prefer a professional to take the calls through active management. Long term investors may also find it cumbersome to constantly shuffle styles and suffer tax leakages if their intent is to reap benefits of long-term investing.

Q4. With the launch of multiple strategies in the newly introduced SIF space, how should investors understand the role of these products within their portfolios? What type of investors are best suited for SIF strategies, and how different are they from traditional mutual fund offerings?

Ans: The SIFs are a new category of mutual fund strategies that are available to investors within the broader MF platform. The investment strategies of the funds utilize the same asset classes and securities as traditional mutual funds - Equity, Fixed Income, Commodities, InVITs, etc. The key differentiator being the manner in which these varied asset classes and instruments ( including derivatives) are used to run the investment strategy for these funds. Investors should evaluate their risk appetite, map out their investment and financial needs and then consider investment choices that would help them achieve these needs. The SIFs tend to run relatively more complex strategies than mutual fund schemes, and for many of the strategies, may have higher risk portfolios. Therefore, investors would be well guided to choose funds based on their risk appetite and evaluate individual SIF strategies for their suitability in their portfolio.

Q5. Many investors struggle with asset allocation discipline during bull and bear cycles. How should investors decide when to rebalance equity exposure rather than reacting emotionally to market movements? What indicators or life-stage factors should ideally drive such decisions?

Ans: Investors should stick to their asset allocations that have been created based on their risk appetite, time horizon and investment needs. Bull and Bear cycles are a normal part of the capital markets and difficult to predict and therefore even more difficult to time investments in accordance with these cycles. We believe investors should review their portfolios on a regular basis and re-balance only if required, based on their needs and risk appetites. It is difficult, but investors should actively try to ignore relatively short-term market movements and stay disciplined and focused on their needs.

Q6. While digital platforms have made investing more accessible, data indicates that investors working with MFDs tend to stay invested longer through market cycles. Do you believe the role of distributors is evolving from product distribution toward behavioural coaching and financial discipline?

Ans: Mutual Fund Distributors are an integral part of the Mutual Fund ecosystem. Financial decisions for most of the populace are a daunting and esoteric activity and therefore most investors require handholding for both the actual investment decisions as well as guidance through the process of executing those investment decisions. As the market grows, evolves and matures, we see distributors playing more active roles in their investors’ investment life cycles. The resilience of SIPs and Mutual Fund flows despite market volatility has clearly shown that the increasing education and emphasis on disciplined investing, staying the course through market cycles and aligning asset allocation to risk appetites is beginning to make an impact on the broader investing population. MFDs have been instrumental in this growth and understanding of investments.

Source: Internal Research

Mutual fund investments are subject to market risks, read all scheme-related documents carefully.